Steiner & Granger: Market review for second quarter 2015

Steiner & Granger

141 N. Main St

P.O. Box 28

Bluffton, OH 45817

419-358-0689

The Markets

As winter weather finally lost its chokehold on the U.S. economy, investors grew increasingly comfortable with the Federal Reserve's slow-and-steady approach to determine when to raise short-term interest rates.

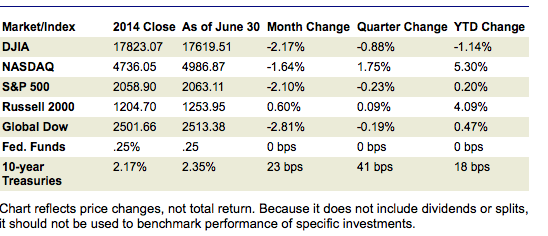

Historic closes were reached by the large-cap Dow (18351) and S&P 500 (2134), while the small-cap Nasdaq (5164) and Russell 2000 (1296) also reached all-time highs during the second quarter. Unfortunately, those gains were all but wiped out as the financial crisis in Greece affected markets domestically and around the world.

Both the Dow and S&P 500 lost 0.88 points and 0.23 points respectively compared to the end of the first quarter. The Nasdaq and Russell 2000 still finished ahead of last quarter, but not by much.

U.S. Treasury prices declined from the first quarter, with corresponding yields making their biggest gains since 2013. The decrease in bond prices was largely attributable to increased consumer spending coupled with investor confidence in the equity markets, which encouraged more money shifting from bonds to equities. Lower unemployment rates along with a slowly improving economy are additional factors leading to lower prices/higher yields.

Oil prices grew to $59 a barrel during the quarter, pushing gas prices higher. Gold, meanwhile, also felt the effects of the global economy, finishing the quarter down at roughly $1,172 an ounce.

Quarterly Economic Perspective

Globally, economic woes in Greece, China, and Puerto Rico serve to illustrate just how fragile the economy is in other parts of the world. The worsening financial crisis in Greece has caused markets to tumble across the globe. The declines came as Greece shut down its banking system and its central bank initiated actions to institute controls aimed at stopping money from leaving the country, which might otherwise cause banks to collapse.

Cash withdrawals are limited to 60 euros ($67) per day, causing long lines at ATMs. With Greece missing its scheduled debt repayment, the odds increased that Greece might exit the eurozone, all of which has prompted the markets to fall as investors were in a sell, sell, sell mode. A voter referendum scheduled for July 5 may determine whether the country will accept financial and economic constraints proposed by creditors, which could lead to continued relief, while a "no" vote could lead to an uncertain financial future for Greece.

China, which has been experiencing favorable market returns for several years, saw its stocks sink the most in five years after reports from several high profile analysts among other analysts warned that valuations had climbed too far, according to Bloomberg. In response to the selloff in Chinese stocks, the People's Bank of China (the country's central bank) cut both its benchmark interest rates and the amount of reserves certain banks are required to hold. All this as the country continues efforts to promote an economy driven by private business and consumer spending rather than infrastructure (government-sponsored) outlays and exports.

Puerto Rico, with its economy ailing, has indicated that it cannot pay its debts. Puerto Rican bond holders are looking at significant losses, as the central government may run out of cash within a month, according to the Wall Street Journal.However, at the time of this writing, Puerto Rico was close to a deal with its creditors to avoid default.

In spite of the latest financial upheaval in Europe, the domestic economy is showing continued signs of improving in the second quarter, following a similar trend begun at the end of the first quarter. Nevertheless, there are still several sectors lagging as described by Federal Reserve Chair Janet Yellen in her June update. Some of the factors that have led the Federal Open Market Committee to refrain from raising interest rates include lagging exports (primarily due to the strength of the dollar), continued weakness in the labor market, and subdued wage growth. In addition, if the global economic tumult hits the United States, the Fed could further delay an interest rate hike.

The revised estimate for the first quarter gross domestic product substantiates Chairperson Yellen's analysis of the economy. Several factors, including unusually severe weather, the West Coast port strike, and the strong dollar, are reflected in the GDP's first quarter contraction of 0.2%. Nevertheless, June's estimate is better than had been reported in May (-0.7%), with exports not lagging quite so far and consumer spending better than first estimated, which may be leading a favorable economy for the latter part of 2015.

In another sign of some economic prosperity, the Department of the Treasury reports that through May, the federal deficit for fiscal 2015 was $365.2 billion--16.3% lower year-on-year. Government receipts were up 9%, although government spending also increased 6%.

The second quarter saw an increase in consumers' income and spending. The Bureau of Economic Analysis reported consumer spending increased 0.9%--the largest increase since August 2009. Income increased 0.5% in May, following a similar 0.5% increase in April. The fact that more consumers are spending is indicative of their growing confidence in the economy. The University of Michigan's Consumer Survey jumped to 97.8--the highest it's been in about 12 years.

Inflationary trends continued on a rather benign track through the quarter, still well below the Federal Reserve's 2% annual target. The Consumer Price Index rose 0.4%--the largest gain since February 2013. However, the increase is primarily attributable to rising gasoline and energy prices. While producer prices increased 0.5% in the second quarter, overall, they are down 1.1% on the year. Generally, annual core inflation has remained between 1.6% and 2% since mid-2012.

Following a slow but steady trend that began toward the end of the first quarter, the housing sector has started to take off in the second quarter. According to the National Association of Realtors, total existing home sales jumped 5.1% in May to a seasonally adjusted annual rate of 5.35 million--9.2% above a year ago. The median existing-home price for all housing types in May was $228,700, which marks the 39th consecutive month of year-over-year price gains. New home sales also increased, moving from 494,000 in March to 546,000 in May--a gain of 10.5%, according to the Census Bureau.

More people are working and fewer are filing for unemployment insurance. The Bureau of Labor Statistics reports that the labor participation rate grew to 62.9%, nonfarm payroll employment increased by 280,000, yet the unemployment rate was essentially unchanged on the year at 5.5%. Jobless claims are at historic lows with initial claims at 271,000 toward the end of June, while continuing claims held at 2.247 million, according to the Department of Labor.

Eye on the Month Ahead

All eyes will continue to focus on the financial crisis in Greece. Will the initial negative impact on the markets in response to Greece's shuttered banks, repayment default, and the prospect of the country's exit from the eurozone continue to drive markets further into negative territory? Will the Federal Reserve provide more information on the timing of the anticipated interest rate hike? Will the dollar increase in strength, further softening domestic exports?

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness.

Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy.

The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. Market indices listed are unmanaged and are not available for direct investment.

Stories Posted This Week

Wednesday, July 2, 2025

Tuesday, July 1, 2025

Monday, June 30, 2025

Sunday, June 29, 2025

Saturday, June 28, 2025

- Community Pool closed June 28

- Weekend Doctor: About Rotator Cuff Repair

- WOAL Swim Champs in Wapakoneta July 11-12

- '60s Survivors Band plays fifth annual free concert

- Bluffton Lions to bring all-abilities playground to new Legacy Park

- July 2025 programs and services at Bluffton Public Library

- Save the date: July 17 Garden Club is all about herbs

- Bluffton Vacation Bible School, July 13-17 at Bluffton Y