Steiner and Granger: Third quarter market review - July to September

Steiner & Granger

141 N. Main St

P.O. Box 28

Bluffton, OH 45817

419-358-0689

[email protected]

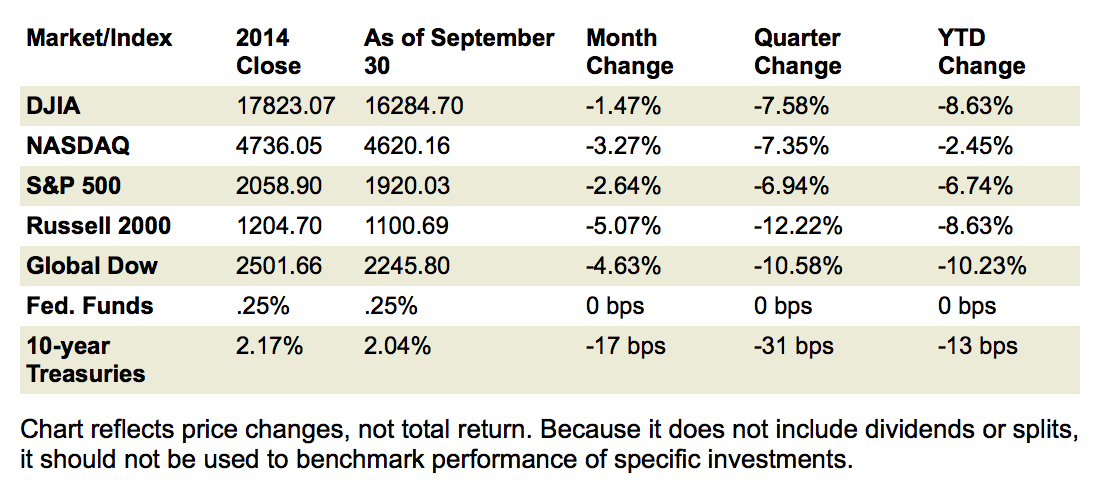

The Markets

Volatility returned to the equities markets in the third quarter, impacted by economic stress in China (the world's second largest economy) and Greece, coupled with underwhelming corporate earnings reports and falling energy stock prices.

While some economic sectors, such as housing and unemployment, offered favorable news, others, including exports and wages, showed little in the way of positive movement.

As a result, the Federal Open Market Committee once again declined to raise interest rates, noting that inflation still hadn't reached the committee's preferred target rate of 2.0%.

Despite a closing rally in the major market indexes listed here, the third quarter ended a tumultuous period in negative territory. The Dow closed the month of September down 243.33 points for the month and 1,334.81 points for the quarter. The S&P fell 6.94% from the close of the second quarter and 6.74% for the year. The Nasdaq dropped 7.35% for the quarter, but only 2.45% for the year--markedly less than the other major indexes listed here. The Russell 2000 and the Global Dow suffered the biggest percentage losses for the quarter, falling 12.22% and 10.58%, respectively.

U.S. Treasuries were not immune to the economic tumult that befell the third quarter. The yield on U.S. 10-year Treasury bonds fell 31 basis points for the quarter. Oil prices (WTI) dropped from $59 per barrel during the second quarter to $46.36 per barrel at the end of the third quarter. Gold, meanwhile, also felt the effects of the global economy, finishing the third quarter at roughly $1,114.50 an ounce compared to $1,172 an ounce at the end of the prior quarter.

Finally, not all falling values are necessarily bad, as the average retail price of a gallon of regular gasoline fell $0.48 to $2.322 at the end of this quarter.

Quarterly Economic Perspective

China's slowing economy sent global markets reeling this summer. Already at its slowest pace in 25 years, China is struggling to reach its target growth rate of 7% for the year.

Adding to concerns about the weakening of the world's second largest economy is the Chinese government's repeated intervention in an attempt to halt a massive sell-off and stabilize its securities market. Interest rates were cut and bank reserve ratios were lowered, allowing for more money to be available to borrow for investment. However, Chinese banks are facing increasing economic risks due to the increasing number of bad loans, further dampening the Chinese economy.

Greece's debt crisis culminated in an agreement with its creditors on an 86 billion euro bailout, which may have allowed the country to remain in the eurozone. Greek Prime Minister Alexis Tsipras, despite campaign promises to write off debt and ease austerity, ultimately negotiated the terms of the new deal, which included stricter austerity measures than had previously existed.

Tsipras subsequently resigned, calling for new elections in September, which resulted in his reelection as prime minister and leader of his left-wing Syriza party. Whether the Greek economy can muster enough support to comply with the requirements of the new debt deal remains to be seen.

The U.S. economy is progressing, but not at a pace sufficient to warrant raising interest rates, according to the Federal Open Market Committee (FOMC). After its September meeting, the FOMC indicated that, while there were improvements in some economic sectors such as labor and the housing market, other areas have lagged, including business and exports.

With inflation still running below the Fed's target rate of 2.0% and the economic uncertainties in China, the FOMC stressed continued patience, yet indicated its expectation that interest rates will be raised sometime this year.

Still revising its second quarter figures, the Bureau of Economic Analysis noted that the real gross domestic product (GDP), which measures the value of the goods and services produced by the nation's economy less the value of the goods and services used up in production, is stronger at an annualized rate of 3.9%. This is up from the prior estimate of 3.7%. The upward revision was attributed to increases in personal consumption expenditures and nonresidential fixed investment.

Exports continue to be a drag on economic growth domestically. According to advance figures from the Commerce Department, August exports fell 3.2% as the trade deficit grew 13.6% to $67 billion.

The Department of the Treasury reports that for the 11-month period ended in August, the federal deficit was $530 billion--$59 billion less than the same 11-month period last year. Government receipts were up 8%, while government spending increased 4.8%.

Showing signs of economic improvement, the third quarter saw an increase in consumers' income and spending. The Bureau of Economic Analysis reported that in August consumer spending increased $52.5 billion, or 0.3%; disposable personal income increased $47.1 billion, or 0.4%; and wages and salaries increased $35.6 billion. The rise in personal consumption compared to the first quarter has spurred GDP growth in the second quarter.

Durable goods orders, or new orders placed with domestic manufacturers for future sales, fell 2.0% in August following a 1.9% increase in July, according to the Commerce Department. However, excluding transportation, new orders decreased less than $0.1 billion, virtually unchanged from a month earlier.

Possibly reflecting the stock market slow-down in September, the University of Michigan's Consumer Survey came in at 87.2 to close the third quarter, its weakest reading since October 2014.

Inflationary trends continued on a rather benign track through the quarter, still well below the Federal Reserve's 2% annual target. Consumer prices fell 0.1% in August, primarily caused by a sharp decline in gasoline prices. Producer prices moved down 0.8% for the 12 months ended in August, the seventh straight 12-month decline. Generally, annual core inflation as of August 31 hovered around 1.83%, not having reached the Fed's preferred 2% target rate since June 2012.

The housing sector remained a favorably trending sector in the third quarter. According to the National Association of Realtors®, total existing home sales in August enjoyed a 6.2% growth rate in year-on-year sales, maintaining a seasonally adjusted annual rate of 5.31 million. The median existing-home price for all housing types remained at $228,700. New home sales were at a seasonally adjusted annual rate of 552,000 in August--5.7% above the July rate of 522,000 and 21.6% above the August 2014 estimate of 454,000, according to the Census Bureau.

More people are working and fewer are filing for unemployment insurance. The Bureau of Labor Statistics reports the number of job openings again rose to a series high of 5.8 million on the last business day of July. The number of hires and separations edged down to 5.0 million and 4.7 million, respectively. The unemployment rate for August stood at 5.1% compared to 6.1% in August 2014. Continuing claims for unemployment insurance in the early part of September came in at 2.24 million compared to 2.46 million a year earlier.

Eye on the Month Ahead

The encouraging start to the third quarter in the securities market proved to be short-lived as September saw stock values tumble. China's economic slowdown continues to dampen investors' enthusiasm. Will concern over the world's second-largest economy impact the Federal Reserve's decision to begin raising interest rates in an attempt to normalize monetary policy in the United States?

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness.

Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange.

The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. Market indices listed are unmanaged and are not available for direct investment.

Stories Posted This Week

Saturday, April 26, 2025

- Kenneth Eugene Mast was head athletic coach for Bluffton College

- Eagle eye over Village Park

- Hillville Rd. barn fire on April 24

- Agenda for April 28 Bluffton Council meeting

- Cory-Rawson High School celebrates Community Day

- Bluffton Senior Center news for May 2025

- Weekend Doctor: The current situation with measles

Friday, April 25, 2025

Thursday, April 24, 2025

- Blanchard Valley Health Foundation welcomes Sapp as Chief Development Officer

- LEO Club invitation to 5K and 1-mile walk & stroll

- Memorial bench and tree planting at Village Arboretum

- Bluffton Beavers sports roundup, April 16-22

- Pirate baseball loss vs. Fort Jennings

- Alan Garmatter is new CNB Chief Credit Officer

- Parks & Recreation Committee meets April 25

- Bad Dreams: Health implications