Steiner and Granger: Third market review

Provided by Jason A. Granger

Steiner & Granger

141 N. Main St., Bluffton

419-358-0689 (Phone)

419-358-8507 (Fax)

Quarterly Market Review: July-September 2016

The second quarter provided a bumpy ride for investors.

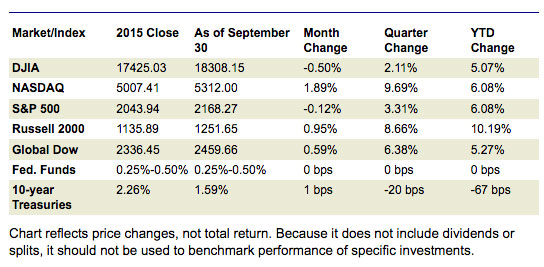

Following the upheaval caused by the Brexit vote in June, July kicked off the third quarter by ending the month in favorable fashion, as each of the indexes listed here posted month-to-month gains, led by the Russell 2000 (5.90%) and the Nasdaq (6.60%).

Stocks held their own for July, despite falling energy shares, as crude oil prices (WTI) sank from around $49 per barrel to under $42 by the close of July. As money moved into equities, bond yields remained on the low side as the yield on 10-year Treasuries remained below 1.60%, closing July at just about where it started at 1.45%.

The dog days of summer saw light trading in August, but that didn't stop the markets from moving sharply. By the middle of the month, the Dow, S&P 500, and Nasdaq had surged to all-time highs — the first time since 1999 that all three indexes reached a new high at the same time.

Yet by the end of August, each of the indexes listed here saw their values fall back to about where they were at the beginning of the month. The large-cap Dow and S&P 500 fell ever so slightly from July's closing values, while the Russell 2000 and Global Dow posted modest gains for the month.

Crude oil fell below $40 per barrel during the month, but rebounded to close the month at about $45 per barrel. Bond prices fell as the yield on 10-year Treasuries reached 1.60%.

For the month, September ended about where it began for equities. Of the indexes listed here, there was relatively little movement during the month, except for the Russell 2000 and the Nasdaq, each of which posted gains for the month close to or over 1.0%.

Overall, the third quarter proved to be a good month for stocks as the indexes listed here posted notable gains, led by Nasdaq, the Russell 2000, and the Global Dow. Long-term bond yields measured by 10-year Treasuries hovered around 1.60% for September, closing the month and quarter at 1.59% — just about where they ended the second quarter.

Gold lost value, closing the second quarter at $1,318.80, down from its June closing value of 1,324.90. Crude oil (WTI) ended the second quarter at about $48.59 per barrel, just about the same price it ended the third quarter ($48.05).

Monthly Economic News

Employment: The employment sector slowed a bit in August, but remained steady with 151,000 new jobs added for the month, compared to 275,000 new jobs added in July. The unemployment rate remained at 4.9% in August — the same as July. There were 7.8 million unemployed persons.

Both the unemployment rate and the number of unemployed persons have shown little movement. Interestingly, the unemployment rate for adult men and adult women was the same — 4.5%. The labor force participation rate remained at 62.8% as did the employment/population ratio, which was 59.7%. According to the latest figures from the Bureau of Labor Statistics, the average workweek decreased by 0.1 hour to 34.3 hours, while average hourly earnings rose to $25.73 compared to $25.59 at the end of July.

FOMC/interest rates: The Fed did not raise interest rates in September, keeping the federal funds target rate at the 0.25%-0.50% range. Following its September meeting, The FOMC's Chair Janet Yellen noted that while a case for a rate increase has strengthened based on overall economic strengthening, consumer price inflation continues to run at a rate that is under the Committee's target of 2.0% and labor market slack is being taken up at a somewhat slower pace than in previous years. Nevertheless, it appears more likely that the Fed will increase rates by the end of the year.

Oil: The price of crude oil (WTI) fluctuated some during September, hovering between $43 and $45 per barrel, finally settling at $48.05 per barrel by the end of the month. The national average retail regular gasoline price was $2.224 on September 26, down from the August 29 selling price of $2.237.

GDP/budget: The U.S. economy is expanding, but at a slow pace. According to the Bureau of Economic Analysis, the final estimate of the second quarter 2016 gross domestic product grew at an annualized rate of 1.4%, compared to the first quarter, which grew at an annual rate of 0.8%.

The primary positives driving the upward movement of the GDP were nonresidential (e.g., business) fixed investment, private inventory investment, and exports. An indicator of inflationary trends, the price index for gross domestic purchases increased 2.1% in the second quarter, compared to an increase of 0.2% in the first quarter.

As to the government's budget, the federal deficit for August was $107 billion, as total receipts came in at about $231 billion and total outlays were $338 billion. The deficit at the end of July was about $113 billion. Through the first 10 months of the fiscal year, the deficit sits at $620.8 billion, compared to $530 billion over the same period last year. The government's fiscal year ends in October.

Inflation/consumer spending: Inflation slowed in August as consumer income and spending increased only marginally. Personal income (pretax earnings) and disposable personal income (income less taxes) each rose 0.2%, while personal spending, as measured by personal consumption expenditures, gained less than 0.1%.

Core personal consumption expenditures (personal spending excluding volatile food and energy costs) rose 0.2% in August, following a 0.1% monthly increase in July. The price index increased 0.2% for the month, and is up 1.0% year-over-year.

The Producer Price Index, which measures the prices companies receive for goods and services, was unchanged in August from July, when prices fell 0.4%. Excluding food, trade services, and energy, prices crept up 0.3% for the month. For the 12 months ended in August, the index for final demand less foods, energy, and trade services moved up 1.2%, the largest increase since climbing 1.3% for the 12 months ended December 2014.

The index for final demand services edged up 0.1% in August following a 0.3% decline in July. The Consumer Price Index, which measures what consumers pay for both goods and services, increased 0.2% in August. Over the last 12 months, the CPI has risen 1.1%. The index less food and energy increased 0.3%.

Housing: The housing market definitely slowed in August. Higher home prices and a lack of available homes for sale are the main reasons given for the drop in the housing sector.

Existing home sales fell 0.9% to a seasonally adjusted annual rate of 5.33 billion, down from July's downwardly revised annual rate of 5.38 billion, according to the National Association of Realtors®. However, existing home sales are slightly ahead of last year's rate of 5.29 billion.

The median sales price for existing homes was $240,200 — up 5.1% from August 2015. Total housing inventory at the end of August fell 3.3% to 2.04 million existing homes available for sale, and is now 10.1% lower than a year ago (2.27 million) and has declined year-over-year for 15 straight months.

The Census Bureau's latest report reveals a fall in new home sales as well. Sales of new single-family homes fell 7.6% in August to an annual rate of 609,000 — down from July's rate of 659,000. The median sales price of new houses sold in August was $284,000, while the average sales price was $353,600. Available inventory of new homes for sale did expand slightly from July. The seasonally adjusted estimate of new houses for sale at the end of August was 235,000. This represents a supply of 4.6 months at the current sales rate, which is up from 231,000 homes available (supply of 4.2 months) in July.

Manufacturing: One of the reasons the Fed has held off on raising interest rates is the continued weakness in the manufacturing and industrial production sectors. The Federal Reserve's monthly index of industrial production (which includes factories, mines, and utilities) fell 0.4% in August after rising 0.6% in July. Manufacturing output also declined 0.4% for the month.

At 104.4% of its 2012 average, total industrial production in August was 1.1% lower than its year-earlier level. Capacity utilization for the industrial sector decreased 0.4 percentage point in August to 75.5%, a rate that is 4.5 percentage points below its long-run (1972-2015) average.

The latest report from the Census Bureau shows new orders for all durable goods (expected to last at least three years) fell $0.1 billion in August from the prior month. Excluding the volatile transportation segment, new orders fell a disappointing 0.4%. Orders for capital goods dropped 4.4%, while shipments fell 0.4%.

Imports and exports: The advance report on international trade in goods revealed that the trade gap narrowed by 0.6% in August. The overall trade deficit was $58.4 billion in August, down $0.4 billion from July. Exports rose 0.7% to $124.6 billion, $0.9 billion more than July exports. Imports jumped 0.3% to $183.0 billion, $0.5 billion more than July imports.

The prices for U.S. imports (goods purchased here but produced abroad) fell for the first time since February, primarily driven by lower fuel prices. August imports sank 0.2% following a 0.1% gain in July. The prices for exports declined 0.8% following four consecutive months of increases. Year-on-year, import prices are down 2.2% and export prices have fallen 2.4%.

International markets: According to the World Trade Organization, world trade will grow more slowly than expected in 2016, expanding by just 1.7%, well below the April forecast of 2.8%.

With expected global GDP growth of 2.2% in 2016, this year would mark the slowest pace of trade and output growth since the financial crisis of 2009. The WTO warned that long-term economic growth could be weakened if growing antiglobalization continues to slow trade.

The Bank of Japan maintained its stimulus policy, hoping to rally equities and spur inflation. Great Britain is still trying to stem its economic slowdown following voters' decision to leave the European Union. More stimulus measures from the Bank of England are expected, including further interest rate decreases.

Consumer sentiment: Despite several weakening economic indicators, consumer confidence gained some momentum in August. The Conference Board Consumer Confidence Index® for August rose 4.5 points to 101.1. On the other hand, the Surveys of Consumers of the University of Michigan Index of Consumer Sentiment dipped from 90.4 in July to 89.8 in August.

Eye on the Month Ahead

Volatility best described the U.S. stock market over this past summer. However, September saw some positive gains overall in equities as the employment sector and consumer spending were positive developments as was news that the Fed would not be raising interest rates during the month.

The FOMC doesn't meet in October, so changing interest rates are not an issue. However, October is particularly important as economic trends for the month will influence the course of action taken by the Fed when it meets again in November.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services).

Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates).

News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations.

All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results.

All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks.

The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy.

The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange.

The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks.

The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide.

The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.