Steiner and Grainger Financial Services: Here's the 2016 annual market review

Provided by Jason A. Granger

Steiner & Granger

141 N. Main St., Bluffton

419-358-0689 (Phone)

419-358-8507 (Fax)

The Markets

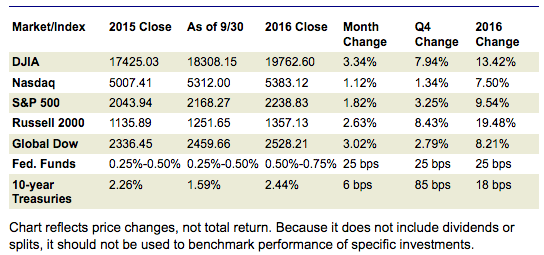

Equities: The year didn't start off well for equities, but by the end of 2016 each of the indexes listed here posted year-over-year gains, some reaching all-time highs. The Dow recorded its best performance since 2013, gaining almost 13.5% from its 2015 closing value. Stocks weathered several financial crises, including China's economic downturn and the Brexit vote.

The large-cap S&P 500 proved less volatile during the year, yet closed 2016 up almost 11.0%. The Russell 2000 proved to be the year's biggest gainer, soaring almost 20.0% over last year's closing value. Most of the gains in equities happened during the second half of the year as favorable corporate earnings, resurgent oil prices, and accelerating consumer income and spending encouraged investors to trade.

Without doubt, the presidential election proved to be a pivot point for the stock market as expectations of looser regulation, fiscal stimulus, and tax cuts fueled the market rally. The Dow (19974.62), S&P 500 (2271.72), Nasdaq (5487.44), and Russell 2000 (1388.07) each attained record-high closing values during the latter part of the year.

Bonds: Volatility best describes the long-term bond market for 2016. Yields on 10-year Treasuries rose for the second straight year as prices fell. The yield on the benchmark 10-year Treasury note closed at 2.44%, up from its 2.26% yield at the close of 2015.

During the early part of the year, bond prices rose as yields sunk below 1.40%. However, as investors saw a strengthening economy, higher inflation, and rising interest rates, a period of bond sales occurred, which peaked during the last quarter when the Treasury yield gained almost 0.85 percentage point, marking the largest quarterly gain since 1994.

Oil: As oil producing countries flooded the market, oil prices fell below $30 per barrel during the first quarter. However, by the end of the year, crude oil prices had achieved their biggest annual gain since 2008. With OPEC pledging to cut production, oil prices surged to almost $60 per barrel, finally settling at $53.89 (WTI) per barrel on December 30.

Currencies: The dollar remained strong throughout the year, affecting imports and exports in the process. Falling oil prices, coupled with the expectation of higher interest rates, helped boost the U.S. dollar, which continued to rise over the course of the year.

The U.S. Dollar Index, a measure of the dollar relative to the currencies of most U.S. major trading partners, gained about 3.67% over last year's closing value. The dollar also benefitted from interest rates abroad, some of which were even lower than those for Treasuries. Tightening trade restrictions proposed by President-elect Trump may curtail continued growth of the dollar in 2017.

Gold: Gold rose over 8.5% on the year, closing 2016 at $1,152.00. Much of the gain was seen during the first half of the year, as the price fell following a lengthy period of sell offs. Gold prices dropped seven of the last eight weeks as the stock market surged.

The Economy

Employment: Improvement in the U.S. job market was slow but steady, with employment growth averaging 180,000 new jobs per month in 2016, compared with an average monthly increase of 229,000 new jobs in 2015.

The unemployment rate ended the year (as of November 2016) at 4.6%, lower than the 5.0% rate at the close of 2015. According to the Bureau of Labor Statistics, there were 7.4 million unemployed persons in November 2016, down from 7.9 million unemployed in November 2015.

The employment participation rate remained relatively the same — 62.7% in 2016 compared to 62.5% at the end of 2015. The employment to population ratio also remained relatively unchanged (59.7% in 2016 to 59.4% in 2015). In 2016, the average workweek was 34.4 hours. Average hourly earnings in 2016 increased $0.62 to $25.89 — a 2.5% gain over 2015.

GDP: The economy maintained a roughly 2.0% average growth rate through the third quarter of 2016. Economic growth has maintained this pace since 2009. The first-quarter GDP rose 0.8%, followed by a 1.4% gain in the second quarter and a 3.5% increase in the third quarter.

Personal consumption expenditures, the value of consumer purchases for goods and services, increased an average of about 3.0% through the first three quarters of 2016. Gross domestic product measures the cost of production of U.S. goods and services. Gross domestic income, which is a measure of all income earned from the production of goods and services, rose 4.8% in the third quarter of 2016, compared to a 2.5% increase in the third quarter of 2015.

Inflation/consumer spending: Based on the growth of consumer income, spending, and inflation, the economy for 2016 may be described as stable at best. Inflation remained below the Fed's stated target rate of 2.0%, but indications are that it is expanding, albeit at a deliberate pace. Personal income through November increased 3.5% compared to November 2015.

After-tax income (disposable personal income) over the same 12-month period rose 3.7%. Consumer spending, as measured by personal consumption expenditures, climbed 4.2% from November 2015. The personal consumption price index, an inflationary gauge relied on by the Fed, rose 1.4% year-over-year, while core PCE (PCE less volatile food and energy prices) increased 1.6%. The prices consumers pay for goods and services saw a moderate 1.7% increase from last November.

Housing: The housing market had been relatively strong for much of the year. Through November, existing home sales are up 15.4% over a year ago. The November annual sales rate of 5.61 million is the highest since February 2007.

The median existing-home price for all housing types in November was $234,900, up 6.8% from November 2015 ($220,000). November's price increase marks the 57th consecutive month of year-over-year gains. Total housing inventory was 1.85 million existing homes for sale — 9.3% lower than last November.

Coupled with a shortage of rental units, home prices and rents are outpacing income in much of the country, according to the National Association of Realtors®. New home sales jumped 16.5% above the November 2015 estimate of 508,000 annual rate of sales.

The median sales price of new houses sold in November 2016 was $305,400 ($317,000 in 2015); the average sales price was $359,900 ($376,800 in 2015). The seasonally adjusted estimate of new houses for sale at the end of November was 250,000. This represents a supply of 5.1 months at the current sales rate compared to a 5.4-months supply a year ago.

Manufacturing: Manufacturing and industrial production were not consistently strong sectors this year. The Federal Reserve's index of industrial production revealed that total industrial production in November was 0.6% lower than its year-earlier level.

Overall industrial capacity utilization, a measure of efficiency, decreased 0.4 percentage point in November to 75.0%, a rate that is 5.0 percentage points below its long-run average. Capacity utilization for manufacturing was 74.8%, a rate that is 3.7 percentage points below its long-run average, which contributed to the decline in overall industrial capacity utilization.

Evidencing stagnant manufacturing activity, new orders for manufactured durable goods (expected to last at least three years) declined 0.3% year-over-year, while shipments fell 0.8%. Capital goods — tangible assets used by manufacturers to produce consumer goods — also fell back as shipments decreased 4.5% and new orders dropped 3.2% from last year.

Imports and exports: For the year, the goods and services trade deficit decreased $8.8 billion, or 2.1%, from the same period in 2015. Exports decreased $58.7 billion, or 3.1%. Imports decreased $67.5 billion, or 2.9%. The strength of the dollar directly affected both import and export prices. Import prices fell 0.1% while export prices dropped 0.3% over the 12 months ended November 2016.

International markets: The big news on the international front was the United Kingdom's referendum vote at the end of June to exit ("Brexit") the European Union.

After the vote was announced, Prime Minister David Cameron, an opponent of the push to leave the EU, resigned, with Theresa May becoming prime minister. Domestically, equities took an immediate hit following news of the vote, but recovered fairly quickly.

The value of the pound remains near a 30-year low and Britain lost its AAA credit rating, increasing the cost of government borrowing. However, both the FTSE 100 and the FTSE 250 closed the year trading higher than before the referendum. Depending on negotiations, the UK is expected to leave the EU by the summer of 2019. In other parts of the world, China's economic growth slowed during the year, but later stabilized following further government stimulus.

Central banks in Japan and Europe continued lowering interest rates to negative values, intending to motivate more lending and investing.

Eye on the Year Ahead

As the year came to a close, the Fed raised interest rates based on some favorable economic news, particularly on the labor front and expanding economic activity. The Fed is expected to consider three more rate increases during 2017. New economic policies promoted by President-elect Donald Trump during his first year in office will likely impact the economy and equities markets, both domestically and abroad.

Will stock prices, which rose dramatically in the weeks following the election, continue their bull run in 2017? Will oil prices reach $60 per barrel as OPEC attempts to curb production? Will the dollar remain strong, impacting import and export prices? Next year may ultimately prove to be as eventful as 2016.

Data sources:

Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services).

Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/ Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates).

News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations.

All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice.

Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks.

The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy.

The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange.

The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks.

The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide.

The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investment.

Stories Posted This Week

Sunday, April 27, 2025

Saturday, April 26, 2025

- Kenneth Eugene Mast was head athletic coach for Bluffton College

- Eagle eye over Village Park

- Hillville Rd. barn fire on April 24

- Agenda for April 28 Bluffton Council meeting

- Cory-Rawson High School celebrates Community Day

- Bluffton Senior Center news for May 2025

- Weekend Doctor: The current situation with measles

Friday, April 25, 2025

Thursday, April 24, 2025

- Blanchard Valley Health Foundation welcomes Sapp as Chief Development Officer

- LEO Club invitation to 5K and 1-mile walk & stroll

- Memorial bench and tree planting at Village Arboretum

- Bluffton Beavers sports roundup, April 16-22

- Pirate baseball loss vs. Fort Jennings

- Alan Garmatter is new CNB Chief Credit Officer

- Parks & Recreation Committee meets April 25

- Bad Dreams: Health implications