Steiner and Granger: First quarter 2016 review

Steiner & Granger

141 N. Main St

P.O. Box 28

Bluffton, OH 45817

419-358-0689

[email protected]

CHECK THE TWO ATTACHMENTS AT THE BOTTOM OF THIS STORY FOR ADDITIONAL INFORMATION RELATED TO THIS ARTICLE.

The Quarter in Review

Employment: The employment sector remained strong with 215,000 new jobs added in March compared with 262,000 at the end of the fourth quarter 2015. The unemployment rate remained at 5.0% in March. There were 8 million unemployed persons in at the end of the first quarter, while the labor force participation rate increased slightly to 63.0% from 62.6% at the end of the fourth quarter.

According to the latest figures from the Bureau of Labor Statistics, the average workweek decreased to 34.4 hours from December's average of 34.5 hours. Average hourly earnings rose to $25.43.

FOMC/interest rates:At both its January and March meetings (it did not meet in February), the Federal Open Market Committee determined that overall economic conditions were not sufficiently improved to justify a further interest rate hike. The last time the Fed increased rates was December, when the Committee raised the target range for the federal funds rate to 0.25%-0.50%.

In support of its decision to maintain interest rates at their present level, the FOMC noted that strong labor market conditions, improvement in the housing sector, and increased household and business spending were offset by slowing economic growth, soft exports, and low inflation, which is continuing to run below the Committee's target rate of 2.0%.

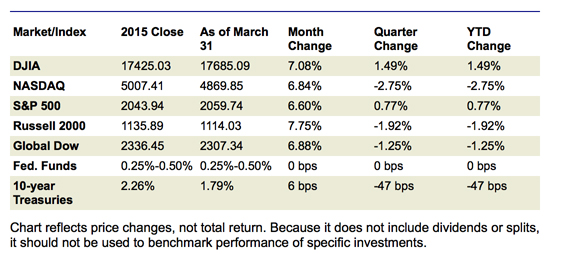

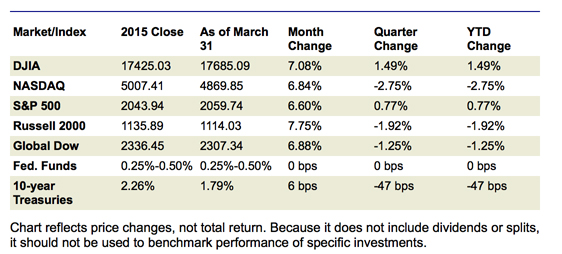

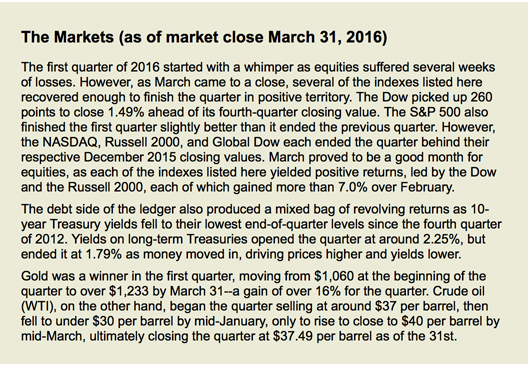

Oil: Oil prices rebounded a bit during the first quarter, although prices remain volatile and relatively low. At the end of March, crude oil (WTI) was selling at $37.49 per barrel compared to December's closing price of $37.07 per barrel. The national average retail regular gasoline price increased during the first quarter of 2016, selling at $2.066 per gallon on March 28, 2016, $0.032 above the December 28 price of $2.034.

GDP/budget: The fourth quarter 2015 gross domestic product grew at an annualized rate of 1.4%, according to the third estimate of the Bureau of Economic Analysis. This is behind the third quarter's 2.0% growth rate and the 3.9% second quarter rate.

As to the federal government's budget, figures can fluctuate significantly from month to month, depending on the timing of payments and outlays. So it's not surprising that the Treasury reported a $192.6 billion budget deficit for February, following January's $55 billion budget surplus. The deficit for fiscal 2016 (October through February) is $353 billion ($386.6 billion for the same period in 2015). Compared to the first five months of fiscal 2015, government receipts are up 5.3%, while outlays are also up 1.86%.

Inflation: Inflation continues to run below the Fed's target rate of 2.0%. In February, personal income (pretax earnings) and disposable personal income (income less taxes) each rose 0.2%, according to the latest report from the Bureau of Economic Analysis.

Personal spending increased only 0.1%. An inflationary indicator of special interest to the Fed, core personal consumption expenditures (personal spending excluding volatile food and energy costs) rose 0.1% in February from the prior month, and is up 1.7% from a year earlier--still short of the Fed's inflation target rate of 2.0%. The Producer Price Index, which measures the prices companies receive for goods and services, decreased 0.2% in February. For the 12 months ended February 2016, final demand prices for all categories of goods and services remained unchanged.

However, over the same period, prices (less food, energy, and trade services) rose 0.9%--the largest 12-month advance since July 2015. Overall, the Consumer Price Index declined 0.2% for February. However, year-on-year, the Consumer Price Index has increased 1.0%. Retail sales were down 0.1% in February over the prior month, but are 3.1% ahead of February 2015.

Housing: The housing market, which has been a strong sector of the economy, may be showing signs of slowing in the first quarter. Sales of existing homes were down 7.1% in February at an annualized rate of 5.08 million, compared to 5.46 million at the end of the fourth quarter. According to the latest report from the National Association of Realtors, year-on-year sales growth of existing homes is up 2.2%.

On the other hand, the median sales price for existing homes was $210,800--a drop of 5.9% from the median price for existing homes in the fourth quarter ($223,200 in December). The latest figures from the Census Bureau show that the 512,000 annual rate of sales of new single-family homes in February was 6.25% below December's revised rate of 544,000. The median sales price of new houses sold in February was $301,400, while the average sales price was $348,900.

Manufacturing: Manufacturing and industrial production have been relatively weak economic sectors. The Federal Reserve's monthly index of industrial production (factories, mines, and utilities) fell 0.5% in February following an 0.8% increase in January. More specifically, manufacturing production increased 0.2% in February, and is up 1.8% over the last 12 months.

Nevertheless, factory production has been hindered by weak exports and low demand for energy equipment. In addition, the latest report from the Census Bureau shows new orders for all durable goods (expected to last at least three years) fell 2.8% in February from January's revised figures. Excluding the volatile transportation segment, new orders fell a disappointing 1.0%.

Imports and exports: International trade in goods showed favorable movement in February as imports were up 1.6% ($181,562 billion), while exports increased 2.0% ($118,698 billion). The difference between the cost of imports and exports increased to $62.9 billion, up slightly from January's revised difference of $62.4 billion. The prices for U.S. imports (goods bought here but produced abroad) fell 0.3% in February following a 1.0% drop in January. The prices for exports dropped 0.4%. Year-on-year, import prices are down 6.1% and export prices have fallen 6.0%.

International markets: The health of China's financial system remains a concern, with large blocks of capital leaving the country on a regular basis. The European Central Bank initiated additional stimulus moves intended to spur the eurozone's economy--and it may be working as economic activity picked up in March, at least according to the latest survey of purchasing managers. However, inflation remains at historically low levels and exports continue to hinder sales.

Consumer sentiment:Consumer confidence seems to have picked up during the first quarter. The Conference Board Consumer Confidence Index® for March rose to 96.2 following February's index reading of 94.0. Consumers expressed favorable views on the labor market and business conditions, but remained concerned with the overall economic outlook.

Eye on the Month Ahead

Economic trends may be more evident as information provided in April will shed more light on the economy and markets. Also, the FOMC meets again in April. when it will once again consider whether economic conditions warrant raising interest rates for the first time in 2016.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates).

News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange.

The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indices listed are unmanaged and are not available for direct investm

Stories Posted This Week

Thursday, November 28, 2024

Wednesday, November 27, 2024

- Happy Thanksgiving from the Bluffton Icon!

- Dec. 6 Handel's Messiah is sold out

- Smoke on the Water: Lung cancer screening guidelines

- Council recap: Village prepares to hire full-time EMS chief, hears "granny flat" legislation feedback

- 2024 Bluffton Blaze of Lights to-do list

- Community Foundation awards $1M in grants